Stock markets hit to their lowest level in 2012 as poor US jobless figures and weak manufacturing data from Europe sparked renewed fears of a global slowdown

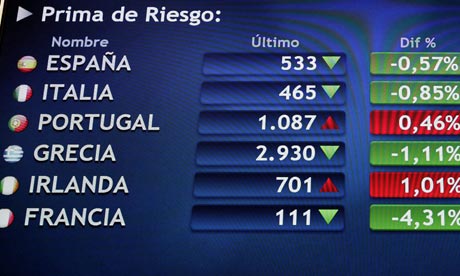

Bond trading - eurozone risk premiums (versus German bonds). Photograph: Sergio Barrenechea/EPA

World markets plunged to their lowest level this year as poor US jobless figures and weak manufacturing data from Europe sparked renewed fears of a global slowdown.

As traders sold off shares in favour of safer assets such as gold, the FTSE 100 in London fell 1.14% to close at 5260.19, its lowest level since 25 November last year. European markets also ended sharply lower, with Germany's Dax down nearly 3.5%, France's Cac down 2.2% and Spain's Ibex off by 0.4%. In the US, the Dow Jones industrial average had fallen more than 220 points - or 1.8% - by the time London closed. After overnight falls in Asia following signs of a slowdown in China, the MSCI world index hit its lowest level since December.

As traders sold off shares in favour of safer assets such as gold, the FTSE 100 in London fell 1.14% to close at 5260.19, its lowest level since 25 November last year. European markets also ended sharply lower, with Germany's Dax down nearly 3.5%, France's Cac down 2.2% and Spain's Ibex off by 0.4%. In the US, the Dow Jones industrial average had fallen more than 220 points - or 1.8% - by the time London closed. After overnight falls in Asia following signs of a slowdown in China, the MSCI world index hit its lowest level since December.Then came the widely watched US non-farm payroll numbers, which showed a rise in employment of just 69,000 in May, compared with forecasts of a 150,000 gain. This was the third set of disappointing numbers, while April's gain of 115,000 jobs was revised down to an increase of 77,000. That prompted an immediate fall in the US dollar against the euro and the yen, with unconfirmed talk the Bank of Japan might have intervened to help stop the slide in the US currency.

All this added to growing fears the eurozone crisis was spiralling out of control. With Spain increasingly in the firing line, the cost of insuring its debt against default hit a record high. The move followed reports that Spain will not announce details of a mechanism to ease the funding problems of its heavily indebted regions today, as hoped.

In Greece left wing leader Alexis Tsipras, gaining ground in the opinion polls ahead of this month's election, ratcheted up his rhetoric against the EU's bailout terms for the country. He repeated his pledge to rip up the bailout agreement if elected, and threatened to take Greece out of Nato.Signs that Ireland had voted in favour of the European fiscal treaty in Thursday's referendum did little to soothe investors' nerves. But gold gained ground, adding around 3% to $1,613 as traders sought safer assets.

With the global economy running out of steam, oil was on the slide, with Brent crude falling more than 3% to $98 a barrel.

No comments:

Post a Comment